Thematic investing: Environment and climate action

The past decade has been the warmest on record, with climate change and an unprecedented loss of biodiversity being the consequences. For nature, animals and humans alike, this is causing drastically restricted living conditions, which in certain instances are already becoming life-threatening for human beings.

The complex and still unknown long-term effects of the novel SARS-CoV-2 virus and its rapid spread show how abruptly familiar living conditions can change. One might argue about whether the virus originated in a market, escaped from a research laboratory in Wuhan, or found its way out of some fur farm in China. But the fact remains that man’s encroachment of the natural habitat of wild animals leads to considerable, previously unimagined risks.

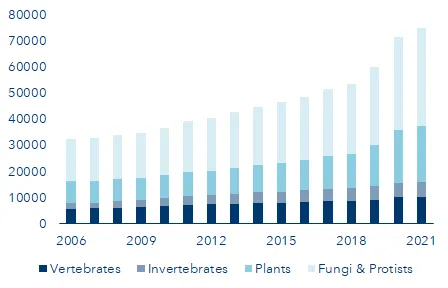

Number of endangered species by groupings

Sources: International Union for Conservation of Nature, VP Bank

The European Investment Bank (EIB) reports having financed with its own borrowings a total of EUR 171 billion in climate action projects between 2012 and 2020. These grants supported a cumulative financing volume of more than EUR 670 billion. Within the framework of the European Union’s newly formulated strategy for biodiversity, the EIB aims to back annual financings of EUR 20 billion through 2030. But given the enormity of today’s challenges, even this sizeable sum is merely a pittance. Paulson Institute, a privately funded US think tank, estimates that there will be an annual financing gap of USD 711 billion if global biodiversity is to be fundamentally maintained. An OECD assessment also underscores the urgency of climate and nature conservation: our natural environment generates an estimated social and economic benefit of USD 125 to 140 trillion per year, or about 1.5 times the global annual gross domestic product (GDP). In manufacturing, about half of the global value creation depends on natural resources.

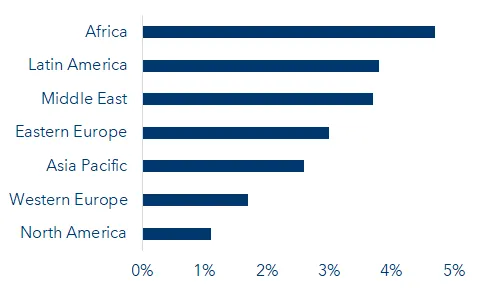

Estimated total economic damage attributable to climate change through 2050, as % of GDP

Sources: Economist Intelligence Unit, VP Bank

Only with a collective effort on the part of the entire global community can sustainable development goals be achieved. The challenges lie primarily in rural and regional structures. Through 2050, the OECD estimates the economic damage from nature degeneration will have amounted to USD 23 trillion, of which climate change alone will account for USD 7.9 trillion according to the Economist Intelligence Unit, a research service by the weekly magazine of the same name. Emerging economies in particular are being disproportionately affected by this trend – most all Africa, where political instability and high population growth pose an especially daunting problem. Thus, it is no surprise that 120 countries have already committed to a net-zero CO2 emissions strategy (for more on CO2 reduction, see the part 3 of this series, “Renewable energies and a circular economy”). And the fact that the German Umweltstiftung is pushing a popular initiative to have nature protection anchored in the Bavarian constitution can only be viewed as a logical consequence. This initiative follows the examples already set by Australia, New Zealand, Chile, Ecuador and even India, all of which have formally granted Mother Nature constitutional rights.

Without water, no life

Of all natural resources, water is arguably the most important. The 2018 United Nations World Water Report predicts that up to 6 billion people will face water scarcity by 2050 as a result of higher water demand, the depletion of potable water resources and increasing water pollution – all driven by economic growth and the rapidly rising global population. By 2050, the demand for food is expected to increase by 60%, thereby putting additional pressure on agriculture which already accounts for 70% of global water demand. An additional 20% is attributable to manufacturing, although this of course varies greatly from region to region. However, particularly in emerging countries which are already plagued by water shortages, industrial water demand is rising disproportionately: an 800% increase is expected for Africa, and 250% for Asia. Globally, the amount of water required for manufacturing alone will quadruple.

Political and societal pressure will increase on multinational corporations that consume disproportionately large amounts of water in emerging nations. This applies to food and beverage companies just as much as it does to mining operations. For example, 65% of potable water consumption in Chile is attributable to the extraction of raw materials, when at the same time natural drinking water supplies have fallen to historic lows.

When it comes to global value creation, three out of four jobs are directly or indirectly dependent on water. Water scarcity (or limited access to it) and pollution have an indirect impact on global economic growth, yet many countries still lack a comprehensive, ecologically sustainable strategy for addressing these problems. Take for example the highly water-intensive agricultural sector, where governments worldwide continue to subsidise environmentally harmful practices at a cost of USD 345 billion per year. According to the British newspaper “The Guardian”, government subsidies amounting to 1 million US dollars per minute are ultimately utilised for fertilisers, deforestation and land cultivation. It is urgently necessary that these funds be redirected.

On a brighter note, solutions to the problem of conserving groundwater reservoirs can be hoped for mainly from technological advances in the field of portable electric power storage units. Intensive research is already being conducted into the use of alternative raw materials such as sodium, silicon, aluminium and zinc. For the foreseeable future, though, lithium will remain a key element of batteries. But there is also promise that research into solid-state batteries will lead to a significant technological breakthrough.

Less is more

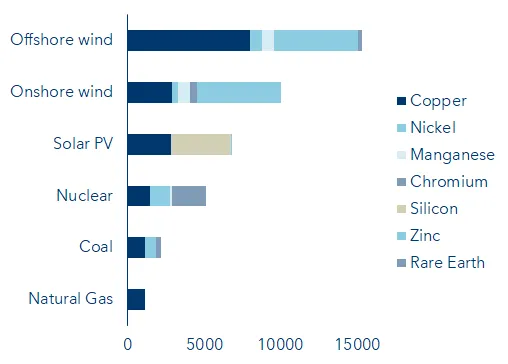

In the quest to progressively replace fossil fuels with renewable energies, electrification has taken centre stage. Photovoltaics, solar and wind energy, electric vehicles and rail transport are central elements of the decarbonisation strategies many countries have adopted. But nothing comes without a cost: the necessary power generation facilities such as solar and wind farms, but also the means to store the energy, create a disproportionate demand for other raw materials. Take for example aluminium, 90% of the demand for which comes from so-called “green industries” due to the important role it plays in the decarbonisation effort. Apart from this industrial metal’s low weight, it is the special physical, chemical and mechanical properties of aluminium that make it so valuable. When alloyed with zinc, silicon or magnesium, it produces up to three times the tensile strength of steel and thus offers solutions for electromobility, the aerospace industry and offshore wind turbines. By 2030, the green transition will have triggered an annual 18% increase in the demand for aluminium. However, producing it is extremely energy- and CO2-intensive and already today accounts for some 2% of all global greenhouse gas generation. Exploding in equal measure is the demand for other raw materials necessary for implementing the net-zero CO2 emissions strategy, namely copper, graphite, magnesium, zinc, cobalt and lithium.

Required raw materials in kg per megawatt

Sources: International Energy Agency (IEA), VP Bank

So at first glance, the fight against climate change is paradoxical – almost like “robbing Peter to pay Paul”. Add to this the fact that the International Energy Agency (EIA) expects the global need for energy to increase by 50% in the coming years. The EIA also notes that two-thirds of the energy produced is actually lost during the production process and/or on its way to end users. The inevitable conclusion: Trying to reduce emissions by simply replacing one energy source with another is not sufficient. A complete industrial overhaul is needed, one that includes not only the efficiency of the regenerative energy mix, but also the way those energies are transported and stored, as well as the direct energy consumption. For a truly transformative change, the International Renewable Energy Association (IRENA) estimates a necessary investment of USD 110 trillion through 2050, 35% of which should be in the area of energy efficiency. As a rather sobering example, today the average efficiency of renewable energies in Europe is about 19%. If the transmission routes are included in this calculation, only about 7% of the primary energy source actually reaches the battery of an electric vehicle. Samsung has achieved an initial breakthrough in the development of solid-state batteries. The company expects this technology to be market-ready by 2025 and afford at least twice the energy efficiency whilst significantly improving the safety of car batteries.

Energy efficiency is a discipline that spans the entire value chain, from power generation all the way through to user consumption. French company Legrand is the world market leader in so-called “smart home” technology, which digitally networks the power grid within a building complex. Comprehensive monitoring of the electricity flow results in a significant reduction of power demand. Another of many examples is provided by Spanish telecom provider Telefonica. By introducing efficient infrastructures, the company has managed to reduce its electricity consumption by 14% since 2015, even though its data transmission volume has increased by 200%.

Industrial progress

The pressing need to adapt is reflected in the infrastructure plans of major economic regions such as Europe, the USA and China. These plans also take into consideration value chains and hence the huge volume of semi-finished products transported between internationally active companies. At present, a carrot-and-stick approach seems to be the way some countries are attacking the problem. With its newly presented initiative “Fit for 55” (i.e. the reduction of CO2 by 55% by the year 2030 compared to 1990), the EU Commission will not only follow through on carbon pricing within the EU, but also impose a CO2 tax on cross-border goods traffic (imports and exports). That’s the stick. Now for the carrot: subsidies will be granted to companies that repatriate the production they previously shifted abroad (optimising transport not only helps to meet climate targets; it also conserves resources).

One of the promising answers from industry is called “additive manufacturing”, in which the processing material is applied layer by layer on-site to create three-dimensional objects. Digital transformation has paved a new route for manufacturers, namely in the form of 3D printing. Highly precise production saves resources and reduces process steps to a minimum. At General Motors, for example, research into additive manufacturing has been a top priority for almost 20 years. Thanks to this, GM has already achieved fuel savings of up to 10% in aircraft engines. Its intensive research and further development in this area is continuing. In addition to the ecological aspects, 3D technology also has economic advantages for General Motors: the industry pays a premium for additively manufactured parts. Since 2003, they have been used in aviation (e.g. in the Boeing 777 and Airbus A350) and, in 2020, Airbus’ unmanned test aircraft “Thor” took off on its own, consisting almost entirely of 3D-printed components. Airbus is using these findings to optimise the weight, design, fuel consumption and production of its aircraft. GM is now applying this know-how to its automobile production: 75% of the 2020 Corvette prototype was manufactured with 3D-printed components. Moreover, spare parts can be produced on-site, thereby eliminating the need for transportation. The process is not yet being used for mass production, but the company expects it will result in manufacturing cost benefits, savings on logistics, and increased flexibility in maintenance and service.

Summary

Relentless climate change and the environmental damage caused by industry paint a very bleak picture for nature and the world we live in. This represents a significant risk to global economic development if no countermeasures are taken. The resolute leveraging of technologies already at our disposal holds the promise of making it possible for the world to successfully confront and halt this trend. And from this industrial transformation process and the resulting changes in consumer behaviour, interesting opportunities open up for medium- to long-term investors.

Please get in touch to your VP-Bank contact for our related investment recommendations.

Important legal information

This document was produced by VP Bank AG (hereinafter: the Bank) and distributed by the companies of VP Bank Group. This document does not constitute an offer or an invitation to buy or sell financial instruments. The recommendations, assessments and statements it contains represent the personal opinions of the VP Bank AG analyst concerned as at the publication date stated in the document and may be changed at any time without advance notice. This document is based on information derived from sources that are believed to be reliable. Although the utmost care has been taken in producing this document and the assessments it contains, no warranty or guarantee can be given that its contents are entirely accurate and complete. In particular, the information in this document may not include all relevant information regarding the financial instruments referred to herein or their issuers.

Additional important information on the risks associated with the financial instruments described in this document, on the characteristics of VP Bank Group, on the treatment of conflicts of interest in connection with these financial instruments and on the distribution of this document can be found at https://www.vpbank.com/Disclaimer_en.pdf