Stocks for the post-Covid economic upswing

The relentless upside move in share prices during the first quarter of 2021 is clear evidence that equity markets are in the process of discounting a return to normal economic conditions. All the classic patterns that characterised previous economic recoveries are on full display: value stocks are now doing better than growth stocks, small-caps are outperforming their large-cap brethren, and inflation concerns are on the rise in response to surging commodity prices and a bump in bond yields. The cycle-driven upside revisions to analysts’ earnings estimates have a high probability of being justified. But the devil is in the details: some of the challenges spawned by the health crisis will not be solved merely by the usual pent-up demand effects.

Today’s clearly euphoric market sentiment can only allow one to presume that the structural changes of late are being underestimated. This applies in particular to sectors such as tourism, aviation, hotels, restaurants and, in this regard, also to parts of the commercial real estate industry. The (forced) adaptability of many service companies in response to the crisis-related mobility constraints speaks volumes: the latest survey conducted by the Global Business Travel Association (GBTA) reveals that 98% of its North American member companies reported having cancelled their international business trips; 92% cancelled all their domestic business travel. The cumulative 2020 revenue shortfall across the travel industry last year amounted to some USD 710 billion in the US alone. Only 27% of the respondents are planning business travel in the next two quarters, and a return to 2019 revenue levels (USD 1.4 trillion) is not expected until 2025. The nimble changeover to video conferencing has engendered a paradigm shift throughout the services industry. After all, companies that used to spend huge amounts to cover travel expenses are now saving a large chunk of those costs. In addition, home officing will play a more significant role going forward. In fact, three out of four US companies want to reduce their office space according to a September survey of 176 CEOs conducted by Fortune Magazine and Deloitte.

Rechannelling reduces catch-up effects

This development alone implies that, by historical comparison, the post-Covid economic rebound will follow different rules. Moreover, states are generously supporting private households either via direct payments or compensation offsets for short-time workers. This has resulted in unexpectedly robust retail sales during the current recession (in the US, the sector recorded a surprising 6.9% growth in revenues for 2020).

But here, too, the devil is in the details: last year, the US online retail segment enjoyed a historic 44% increase in sales to USD 861 bn, even as 17 bricks-and-mortar retailers filed for bankruptcy. The latter employed around 274,000 people and generated cumulative revenues of just over USD 44.5 bn in 2019. To a certain degree, the shift to online retailing diverts the net value added of intermediary merchants away from the domestic market and into the country of production, ergo the ongoing economic boom in China. In previous upswings, the catch-up effects from heightened consumption were pivotal. Less impetus can be expected this time around.

The wise follow the authorities

For better or worse, digitalisation showed where the journey is heading. The pandemic has made it woefully clear how ill-prepared not only companies but also the authorities are for the digital future. The retail sector demonstrated its agility right from the start, but there are enormous deficits in terms of home-officing, digital healthcare and online education.

The very nature of viral proliferation means that Covid-19 and its mutations will be with us for years to come. By the same token, digitalisation stands out for the heightened productivity, employee motivation and significant cost savings it offers. Thus the odds are great that more extensive investments will be directed towards accelerating the digital transformation in the near future.

In this respect, governments are making quite clever use of today’s crisis. But the achievement of their well-intended, strategically motivated goals goes hand in hand with an increase in national debt. Despite the existing burdensome debt levels, few objections are to be heard. However, in addition to their resolute efforts to create a climate-neutral industrial environment, the nations will also need to provide medium-sized companies with financial support aimed at digital modernisation.

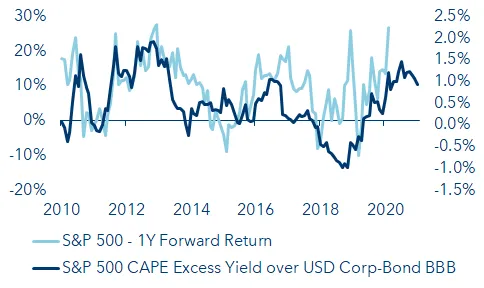

Equity markets still afford attractive opportunities

An unusually high number of infrastructure projects across large reaches of the manufacturing and service landscape will by necessity lead to huge capital expenditures in the coming years. In many sectors, this will propel corporate profit growth and thereby offer interesting opportunities for medium- to long-term orientated investors. Today’s already lofty valuations will be relativised by those increased earnings and the related growth rates should cushion the otherwise retarding effects of rising interest rates. Equally spoken, the pace of share price gains can be expected to decrease. After all, when the forecasts for inflation-adjusted corporate profit growth in the US are taken into account, the earnings yield is only 0.6% above the comparable yield on ten-year corporate bonds.

In Europe, this relationship is significantly higher at 4.6%. Thus it is advisable to continue favouring companies with strong balance sheets, as well as to focus on positive cash flow trends spanning two to four years. Also promising are companies that have already done their “digital homework” or intend to embrace digital transformation in the next two to three quarters, as such endeavours trigger positive effects in terms of profit margins.

With these aspects in mind, we have selected for your consideration the most promising companies in the USA, Europe, Switzerland and the Nordic countries.

Please contact your VP Bank client advisor for more information.

Important legal information

This document was produced by VP Bank AG (hereinafter: the Bank) and distributed by the companies of VP Bank Group. This document does not constitute an offer or an invitation to buy or sell financial instruments. The recommendations, assessments and statements it contains represent the personal opinions of the VP Bank AG analyst concerned as at the publication date stated in the document and may be changed at any time without advance notice. This document is based on information derived from sources that are believed to be reliable. Although the utmost care has been taken in producing this document and the assessments it contains, no warranty or guarantee can be given that its contents are entirely accurate and complete. In particular, the information in this document may not include all relevant information regarding the financial instruments referred to herein or their issuers.

Additional important information on the risks associated with the financial instruments described in this document, on the characteristics of VP Bank Group, on the treatment of conflicts of interest in connection with these financial instruments and on the distribution of this document can be found at https://www.vpbank.com/legal_notes_en.pdf