The Fear of missing out

Whether economic indicators, stock markets, oil prices, inflation or interest rates: there is confidence across the board. The stock markets are up compared to the beginning of the year, some like the German leading index Dax have even reached record highs. The explosion of the shares of Gamestop, a US computer game retailer, caused worldwide headlines. Even though this episode is behind us, it serves as proof that financial markets are prone to exaggerations.

If we look at valuation and sentiment indicators, they show the broad and growing confidence. The US equity market, for example, is trading at a 2021 price-to-earnings (P/E) ratio of above 30 and risk appetite has climbed to its highest level since the end of 2017, according to an indicator from the US investment bank Goldman Sachs. The recent rise is spurred by the prospect of a new stimulus programme in the US.

However, this pronounced appetite for risk has a downside: if too many investors feel they are missing out, short-term exaggerations may occur. This is better known as the "Fear of missing out".

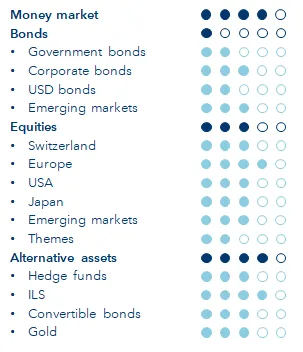

Therefore, care should be taken to protect the portfolio from setbacks. To this end, we increased our position in insurance-linked securities in February, as these have proven to make the portfolio resilient. In addition, we are focusing regionally on European equities, as these are comparatively attractive in terms of valuation. Despite all this, however, our positioning is clear: the portfolio is geared towards the upswing.