What awaits us after the US presidential elections?

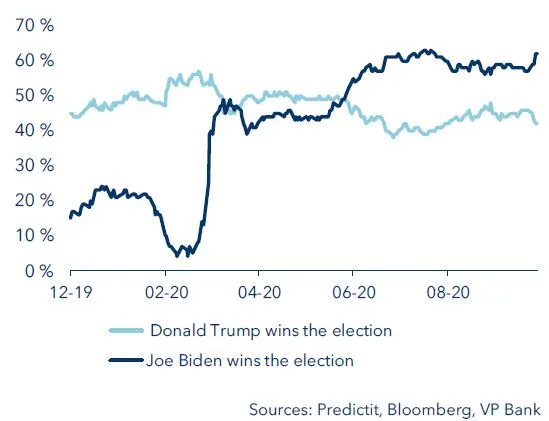

The ultimate outcome of the US presidential election is uncertain. Democratic challenger Joe Biden currently leads in the polls, but those findings may be misleading – this because in reality the elections are decided in the so-called battleground (or “swing”) states such as Arizona, Florida, Michigan, North Carolina, Pennsylvania and Wisconsin where there is no traditional majority for one or the other party. If the latest polls are to be believed, Biden leads in all of these states, but his edge over incumbent president Donald Trump is not wide enough to make the election already a done deal. However, the odds of winning the election have recently shifted back in favour of Joe Biden, after the Democratic challenger had lost his lead in August and September. But it remains open who will win the election on 3 November. However, Joe Biden enjoys a strategic advantage in view of the White House's inadequate crisis management in the Corona affair.

Betting odds: Who will win the election?

The Biden agenda: higher taxes and a green economy

Democrat Joe Biden entered the race for the Oval Office with a broad economic agenda. Biden’s strategic aim is to score points with voters on the basis of his competence in economic policy. Essentially, he is stressing three major points; namely, reversing the Trump administration’s tax cuts, launching a large-scale infrastructure investment programme, and giving the economy a pronounced “green tint”.

All these points hinge on a change in the values and mindset in broad swathes of American society. The Democrats are convinced that their agenda is currently well positioned with this transformation concept. The equal treatment of women and men as well as America’s various ethnic groups, the widening wealth gap and climate change are all hot-button issues. And in addressing them, the Democrats are counting on more government say-so. For example, a recent Gallup poll reveals that 47% of Americans are now in favour of strengthening the public sector if the effort to solve social problems. In 2010, the same survey showed a reading of only 36%. With his program, Biden wants to leverage this changed view. Specifically, he plans involve:

Tax hikes

If elected president, Biden intends to reverse Trump’s 2017 Tax Reform Act, which massively lowered taxes as a way to extend the already long-running economic recovery in America. The Democrat would also like to make top earners and companies pay more: the highest marginal tax rate on income will increase from 37% to 39.6%, and tax loopholes are to be minimised. Under Biden’s plans, the corporate tax rate will increase from 21% to 28%. However, this burden is still significantly less than before Trump reduced it from 35%. In addition, companies that earn profits of USD 100 million or more will be subject to a tax of at least 15%, and the shifting of corporate profits to low-tax countries is to be made more difficult. To this end, the tax on a portion of the profits of US companies’ foreign subsidiaries (Global Intangible Low Tax Income, GILTI) would be doubled to 21%. In turn, the increased government revenues are earmarked for providing greater relief to low-income earners and ensuring a more equitable distribution of wealth.

Investment programme as a boost to the economy

“Build Back Better” is the name Joe Biden attaches to his gigantic infrastructure investment program. USD 400 billion is to flow into government contracts for infrastructure projects and procurement. A further USD 300 billion is earmarked for investment in research and development projects in biotechnology, telecommunications and artificial intelligence. The candidate claims that this programme will create some five million new jobs in a labour market that has taken a heavy hit from the coronavirus crisis.

A “green economy”

The country’s electrical power supply should be CO2-neutral by 2035. Here, Biden is counting on cooperation between the public sector and private investors. In addition, there will be incentives for energy-efficient cars and home appliances. The insulation of houses is also to be subsidised.

Trade conflicts as well

Those hoping for a change of course in US trade policy are likely to be disappointed: Joe Biden is touting “Buy American”. The Democrats, too, take a dim view of the unfair conditions in trade with China. In fact is was Democratic senators who originally called on the US president to take a tougher stance on Beijing. The direction is therefore clear: Biden will also take China to task. However, it can be assumed that the tone will be much more conciliatory than the Trump approach, something that should make negotiations with Beijing more productive.

Biden is a self-proclaimed Transatlantic advocate. Good relationships with America’s European allies are important in the mind of the Democrat. This is good news for the European car manufacturers as they would have less to fear from Washington in future. Dealings in general with Europe should turn out to be more amicable.

The Trump agenda: America first

The Republicans have no official election platform – the name “Donald Trump” alone suffices, and the president’s “America First” credo continues to take centre stage. So his re-election would mean more of the reality show we have been forced to watch in the past four years. The centrepiece of the new/old president’s stage performance would be a “fairer” trade policy. Disputes with China and America’s European trade partners are as good as pre-programmed. The current low tax regime would remain in place, and Trump would seek regulatory relief for corporate America. The same applies to environmental regulations.

Who can spur the higher growth?

To state it right up front: Although different in nature, the policies of both Trump and Biden harbour positive as well as negative growth impulses. In principle, a continuation of Trump’s low tax regime argues for higher GDP growth compared to the programme proposed by Joe Biden. However, as the past four years have shown, trade conflicts spawn uncertainty, which in turn weighs on corporate capital spending throughout the world. That harms not only the US economy, but the global economy as a whole.

Biden’s planned economic programme has the potential to spur growth significantly. But if support from the Senate fails to materialise due to a post-election continuation of the existing Republican majority in that chamber of Congress, there will be no meaningful increase in state spending. And second, if tax increases are implemented at the same time as his ambitious programme, Biden’s envisioned measures could possibly turn out to be a brake on growth. On the other hand, a more conciliatory tone vis-à-vis trade partners, which is to be expected from a Democratic administration, would ensure less acrimony on the international stage. As a result, companies would have greater planning certainty and thus be more inclined to invest in capital goods.

Since the two candidates could hardly be more different in character and their agendas include both growth-promoting and growth-retarding aspects, we believe the ultimate the impact on overall economic growth rates will turn out to be “neutral”.

Effects on the US dollar

Regardless of who comes away the winner on Election Day, the greenback is likely to remain soft for the time being due to its present overvaluation. The return trip to fair-value levels has begun. In principle, the huge-volume investment programme Joe Biden envisions would argue for a further widening of the US budget deficit. Given what is also a shortfall in the current account, this would result in a substantial twin deficit, which in turn would weigh on the value of the dollar.

However, Biden needs the support of Congress. If the Democrats fail to gain a majority in the Senate, the investment programme will be dead on arrival. By the same token, if Biden at least partially reverses Trump’s tax cuts and no significant increase in government spending were to happen, the result would be budget consolidation. Biden would thereby follow in the footsteps of his Democrat predecessors. Contrary to the widely held belief that Democrats are bigtime spenders and Republican prudent penny-pinchers, the opposite has actually been the case in recent decades: in phases when a Democrat has occupied the Oval Office, the budget deficit has been reduced (see an in-depth assessment of the US dollar in VP Bank’s investment magazine “Telescope”)

Against this backdrop, we would expect to see over the long term a stronger US dollar under a Biden administration than under another Trump presidency. However, a potential upside move in USD is unlikely to materialise until some point during the old/new president’s next term of office. In the meantime, the Fed's accommodative monetary policy and the huge US budget deficit suggest that the greenback will continue to lose ground.

Effects on monetary policy

The course of US monetary policy has been set until further notice – regardless of the president and his policies. The economic aftershocks from the coronavirus pandemic will persist for some time to come. A higher unemployment rate compared to the pre-COVID-19 period makes any attempt at significant wage increases a no-go. And without rising wages, any thought about a sustained increase in inflation is illusory. Looking beyond the immediate horizon, the following can be expected to hold true: the occupant of the Oval Office will not have any significant influence on monetary policy, in that the growth effects from the foreseen programmes of either candidate are neutral in our view. Hence, the US presidential election should also be largely neutral for the long end of the yield curve; in other words, we reckon that yields on 10-year Treasuries will not be reflective of any person-specific trend. However, if re-elected, Trump could continue his verbal attacks as a way of pressuring the Fed to adopt an even looser monetary policy.

Effects on the crude oil market

Trump is considered an ally of the American crude oil industry. By having approved further drilling on federal lands and the liberalisation of pipeline and export projects, he played a significant role in America’s emergence as the world’s largest crude producer. Trump is also considered a force to be reckoned with in the global oil market, where he had the audacity to publicly criticise decisions of OPEC. Moreover, he recently acted as a mediator between Russia and Saudi Arabia in effort to stabilise oil prices. Sanctions against Iran and Venezuela have also exerted a notable influence: since the buyers of crude oil from those countries must expect to incur economic sanctions from the United States, their current production volumes are well below the previous highs.

Owing to the COVID-19 pandemic, the American oil industry is currently in a precarious situation, which is why some companies have already been forced to file for Chapter 11 bankruptcy protection. Presumably, Biden would not take any active measures against the crude oil sector at least for the time being, even though he wants to pave the way for an energy transformation in the USA. Be that as it may, if Biden is elected, the American crude oil sector can expect less support from the White House. While we rule out the possibility of a ban on fracking and US exports, no new drilling permits are likely to be issued for exploration on federal lands. A Biden victory could therefore have a negative impact on the oil sector’s capital spending, production volumes and tax contributions over a lengthy period of time.

Effects on the equity markets

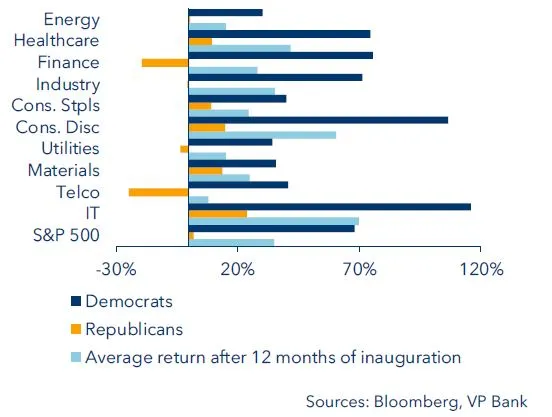

The debate surrounding the US presidential election is not limited to the media – the topic is also controversial among investors. The two major parties are being associated with one or another lobby. However, a look at stock performance in the twelve months after a given president takes office or over his entire reign reveals the unexpected: namely, Democratic presidents have paid off better for investors not only in terms of the market as a whole, but also along sector-specific lines. This tendency, at least as it pertains to the S&P 500, can be observed all the way back to 1929 (sector-specific data have only been available since 1997, when Bill Clinton began his second term of office).

Total returns on US stocks during presidencies since 1997

Health crisis is a burden

The dark cloud of the global health crisis looms over America’s upcoming Election Day. The related negative effects on the economy are so immense that the necessary countermeasures will no doubt have an influence on the proposed measures of the current/new government for years to come. Similar yet different situations were already observable in 2001 after the bursting of the dot.com bubble and in 2009 following the great financial market crisis. In the end, politicians’ reaction, regardless of party allegiance, was opportunistic. Today, it is the healthcare sector that is receiving strong attention from Democrats and Republicans alike. Thus is can be expected that access to health services will be made more available (and affordable?). While Biden wants to optimise the system via regulations in keeping with Obama’s Affordable Care Act, Trump wants that free-market forces resolve the problem. Whatever the case, lower prices for prescription drugs are in the interest of both candidates. The major pharmaceutical companies will face structural headwinds, whilst businesses involved in drug research and telemedicine can expect advantages.

Climate policy could hardly be more different

The two candidates differ greatly in their stance on climate-related issues. Trump’s strategy in this regard, focused as it is on the traditional energy sector, has failed miserably until now, with the coronavirus crisis making things even harder for the sector. The incumbent is hard put to address the matter of renewable energies, and, as evidenced by his decision to withdraw from the Paris Climate Accord, he is too dismissive of the findings on global warming. Biden, for his part, views this as the very linchpin of the next economic cycle. With a budget of USD 2 trillion over the next four years, he intends to drive the development of climate-friendly infrastructure, as well as alternative fuels (electromobility, green hydrogen and biomass) and the equipment necessary to make them. Also a part of his agenda is the expansion of capacities in the field of solar and wind energy. Trump counters this with his vision of space travel, which includes the launch of a manned space flight to Mars via a fixed base on the moon. Here, his strategy counts on the strong involvement of the private sector.

Equity investors: The tax policy matters

Income tax policy represents the third important aspect for equity investors, and here the agendas of the two candidates also diverge. This is a crucial matter, as it has an impact on consumption. Private spending has been the most stable and important factor for the US economy in recent years and above all in the current crisis-fraught year. Trump is aiming for a middle-class tax cut. For Biden, this is not enough. He sees more sense in narrowing the income gap. He wants to achieve this through higher taxation of top earners and a significant increase in the minimum wage. If Biden succeeds in this, a considerable increase in consumer spending is likely to result – a strategy that would give a boost especially to the US domestic economy. For investors, though, this comes with a somewhat sour aftertaste. Higher labour costs and rising corporate taxes would weigh on profits from 2022 onwards, not necessarily the best of news for shareholders. Trump, on the other hand, would stand by the corporate tax rates he lowered already in 2018.

Summary

Incumbent US president Donald Trump and his challenger, Joe Biden, represent fundamentally different economic principles. Both election platforms harbour positive as well as negative elements in terms of economic growth. Nonetheless, the current COVID-19 pandemic and low interest rates remain the key influencing factors. History shows that Democratic presidents tend to be more beneficial for investors in US stocks. That said, Biden’s corporate tax plans could cause the stock market to react cautiously at first to a victory by the Democrats. However, this could change in the medium term. Already existing trends in the area of digitalisation would be spurred by the additional spending on infrastructure and research. These investments would mainly have the effect of filling the order books of American companies. Whether they are aimed at bringing about a climate-friendly future or merely maintaining America’s otherwise ageing infrastructure is of secondary importance. From the perspective of European companies, Biden would probably be the more preferable.

Just how many accents the next president can really set in the coming years, though, essentially depends on the composition of Congress – and here, the race for a Senate majority is a nail-biter. If the president lacks that majority, compromises will have to be made in order to avoid blockage of key legislation.

Oddly, anything that complicates the political work of the next president would probably represent the best scenario for the financial markets, only because of the decreased potential for political experiments; in other words, continuity would be ensured.

The arguably worst scenario would be an initially unclear election result (due to a high proportion of mail-in/absentee voters) and/or an outcome that is then not recognised by Donald Trump. This would probably result in weeks of legal disputes and only be put to rest when the Supreme Court rules on the final result. Such a brouhaha would not only create uncertainty in the financial markets, but also poison the political climate and divert attention away from today’s daunting economic challenges.

Consequently, investors should pay attention not only to who becomes the next US president, but also how clear-cut the voting result is and which party ultimately holds a majority in the two chambers of Congress.

Important legal information

This document was produced by VP Bank AG (hereinafter: the Bank) and distributed by the companies of VP Bank Group. This document does not constitute an offer or an invitation to buy or sell financial instruments. The recommendations, assessments and statements it contains represent the personal opinions of the VP Bank AG analyst concerned as at the publication date stated in the document and may be changed at any time without advance notice. This document is based on information derived from sources that are believed to be reliable. Although the utmost care has been taken in producing this document and the assessments it contains, no warranty or guarantee can be given that its contents are entirely accurate and complete. In particular, the information in this document may not include all relevant information regarding the financial instruments referred to herein or their issuers.

Additional important information on the risks associated with the financial instruments described in this document, on the characteristics of VP Bank Group, on the treatment of conflicts of interest in connection with these financial instruments and on the distribution of this document can be found at https://www.vpbank.com/legal_notice_en

Add the first comment