The virus has not been defeated yet

The price of gold has continued its run and easily passed both its all-time high and the USD 2,000 mark per troy ounce. Since the beginning of the year, this has resulted in an increase of more than 30% in US dollar terms. That the price has eased somewhat in recent days is not untypical after such a strong and rapid rise. We read this development as a breather rather than a change of the price trend.

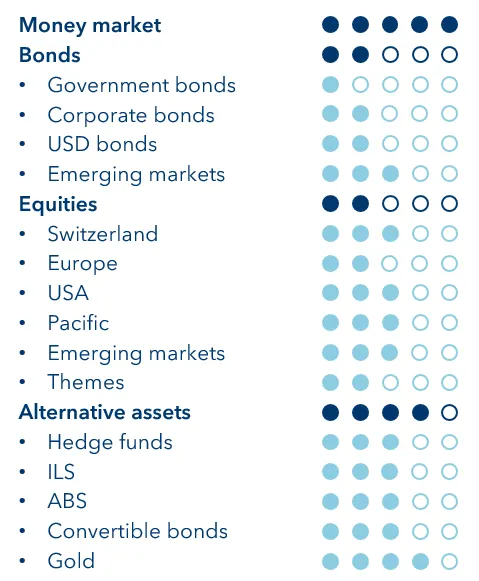

From our point of view, gold is receiving support from various sides: be it from the weakening US dollar, the negative real interest rates or the anxiety of many investors that inflation could rise in the long term after all. Last but not least, we appreciate gold's very good diversifying properties and therefore stick to our long-standing gold positioning.

As much support as we are currently seeing for gold, the US dollar is receiving little or none of that. The greenback is currently facing headwinds. Since we published the first issue of our “Telescope" magazine entitled “The Wimpy Dollar" at the end of May, the US dollar has weakened across the board. As we explained in detail in the magazine (link here), there are good reasons to believe that this was only the prelude to a longer-term phase of dollar weakness. That is why we continue to consistently hedge the US dollar.