No change of direction expected after Germany’s federal election

The German federal election on 26 September has developed into an exciting race, but the outcome will not bring any fundamental change in Germany’s political agenda. The problems are clear, and important policy directions have already been set. All the parties are faced with the same basic issues, so room for manoeuvre is very limited. The goals are broadly agreed – discussion is about how to achieve them. The most important tasks confronting the next government are as follows. All will require a massive input of resources.

- A complete phase-out of coal-fired electricity generation by 2038 at the latest. This goal is a done deal. All the political parties except the right-wing Alternative for Germany (AfD) are committed to it.

- All the parties have promised to speed up the development of the country’s digital infrastructure. This includes the digitalisation of public administration.

- Industrialists regard German bureaucracy as a major business risk. Surveys by the Association of German Chambers of Industry and Commerce regularly highlight this concern. All the parties except the far-left “Die Linke” (The Left) have addressed this problem in their manifestos and aim to create slimmer and more efficient administrative structures.

- The consequences of demographic change are becoming increasing visible. There is a shortage of care-givers, and the future financing of the social insurance system is still an unresolved problem.

If climate objectives are to be achieved, Germany’s coal-fired power stations will have to be closed down. According to the Federal Statistical Office, coal’s share of electricity generation in 2021 (a low-wind year so far) has been 27%. But within 17 years from now, Germany’s entire electricity supply must be derived from alternative energies. This enormous challenge will overshadow many other political objectives.

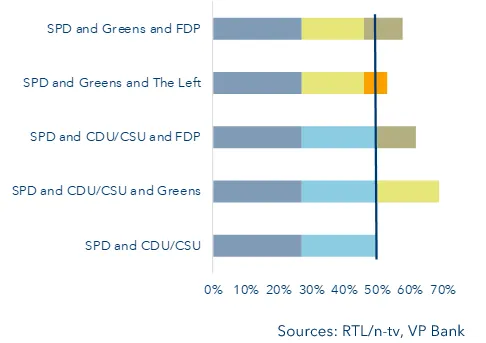

Coalition options

The latest opinion polls put the Social Democratic Party (SPD) in the lead. The SPD has bounced back impressively in recent weeks under its chancellor candidate Olaf Scholz, who is finance minister in the current coalition government. In second place comes the centre-right CDU/CSU alliance (the Christian Democratic Union of Germany and its Bavarian sister party the Christian Social Union ), followed by the Greens, the liberal Free Democratic Party (FDP) and the AfD. Electoral victory for the SPD therefore now looks likely. This is underlined by voters’ response when they are asked who they would choose if they could elect the chancellor directly. According to a survey by the RTL/n-tv media group, Olaf Scholz gets a vote of 30%, the Greens’ candidate Annalena Baerbock 15% and the CDU candidate Armin Laschet only 9%.

If the SPD secures the largest share of parliamentary seats on 26 September, the latest polls suggest that there would be three possible coalition options: an alliance with the Greens and the FDP (“traffic light coalition” – red, yellow, green), a left-wing coalition with The Left party and the Greens or a coalition with the CDU/CSU and FDP.

Possible coalition options on basis of current opinion polls

The likeliest outcome in our view is a traffic light coalition. Scholz has recently said he would not countenance a leftward lurch under his chancellorship, though he admittedly did not explicitly rule out a government role for The Left party. Scholz is a middle-of-the-road politician, so a link-up with The Left is hard to envisage. The fact that he has not categorically rejected the possibility can be seen as a sop to the left wing of his own party. If the SPD does win the election, he can be expected to show his hand and come out more firmly against a left alliance. In any case, the differences between the SPD and The Left on defence and foreign policy present an almost insurmountable obstacle. The Left is opposed to NATO. It has recently signalled some flexibility on this point as the price of a place in cabinet, but it also opposes any increase in defence spending. The SPD, however, wants to modernise Germany’s armed forces, which could involve a bigger defence budget. Thus an alliance with The Left is intrinsically difficult.

The possibility of a new "grand coalition", that is, an alliance of CDU / CSU and SPD, is on shaky ground. Based on current surveys, there would theoretically be a wafer-thin majority for a new edition of the "Great Coalition". Germany has been governed by a grand coalition (dubbed a “Groko” in German) since 2013, but such an arrangement always looks like an emergency makeshift and is disliked by politicians as well as by the public at large. So a “Groko plus”, i.e. including the FDP, is also not viewed with favour by any of the chancellor candidates. The same goes for a coalition of the SPD, CDU/CSU and Greens (known as a “Germany coalition”). Here again the similarity with a grand coalition would be too strong.

What about the chances of the CDU/CSU forming a government without the SPD even if the latter emerges as the largest party? We can only see happening if a victorious SPD were to fail in its attempt to build a coalition. In that case the CDU/CSU might try to form a “Jamaica coalition” (black, yellow, green) by getting into bed with the Greens and the FDP.

Implications for the financial markets

As most elements of the political agenda are predetermined (notably the transition to green energy and accelerated digitalisation), we do not foresee any abrupt change of direction in German politics as a result of the election. The only outcome that would lead to a major policy shift would be a left-wing alliance including The Left, which would probably lead to a major expansion of the public sector, tougher regulation of corporations and the financial markets and rising government debt. This last point could bring Germany into conflict with the EU, paving the way for debt pooling and a destabilisation of the euro.

But if The Left is not brought on board, the election outcome is unlikely to have any significant impact on the financial markets. Priorities are already set in stone, fiscal room for manoeuvre is limited by the debt mountain resulting from the pandemic, and all the possible government participants are supportive of the EU and the euro.

Conclusion

The new government will face an almost unprecedented catalogue of challenges. The “to do” list will prioritise green energy transformation, digitalisation of the public domain and measures to deal with the consequences of demographic change. The objectives are agreed, and action cannot be postponed. Other policy goals will hardly get a look-in. German politics are therefore not on the verge of a major upheaval. However, with the departure of Angela Merkel the EU loses a powerful mediator and conciliator. Future conflicts will require increased cooperation between Germany and France. We do not expect the election to have significant consequences for the financial markets.

Important legal information

This document was produced by VP Bank AG (hereinafter: the Bank) and distributed by the companies of VP Bank Group. This document does not constitute an offer or an invitation to buy or sell financial instruments. The recommendations, assessments and statements it contains represent the personal opinions of the VP Bank AG analyst concerned as at the publication date stated in the document and may be changed at any time without advance notice. This document is based on information derived from sources that are believed to be reliable. Although the utmost care has been taken in producing this document and the assessments it contains, no warranty or guarantee can be given that its contents are entirely accurate and complete. In particular, the information in this document may not include all relevant information regarding the financial instruments referred to herein or their issuers.

Additional important information on the risks associated with the financial instruments described in this document, on the characteristics of VP Bank Group, on the treatment of conflicts of interest in connection with these financial instruments and on the distribution of this document can be found at https://www.vpbank.com/legal_notes_en.pdf