Dislocations & Opportunities in the Fixed-Income market (guest article)

The underlying changes in the global economic and geopolitical landscape revealed several dislocations in the Fixed-Income market, with the repricing of risk opening the doors to yield-seekers. By combining in-depth fundamental analysis and comprehensive assessment of the risk-reward profile, we explore the current sea of opportunities and seize the most attractive yields backed by sustainable financials.

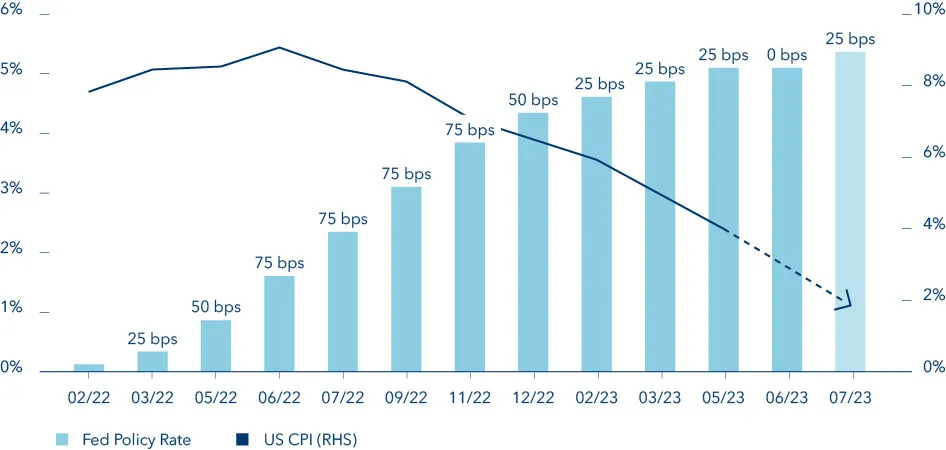

Shortly before the peak

After observing prices soar to heights not seen in decades, central banks intervened by rapidly raising interest rates. In the US, the Fed has now reached a median target rate of 5.125%, which the market expects to be around 5.375%, although Fed Chair Powell has indicated that further hikes may be needed, implying a final rate of 5.50%.

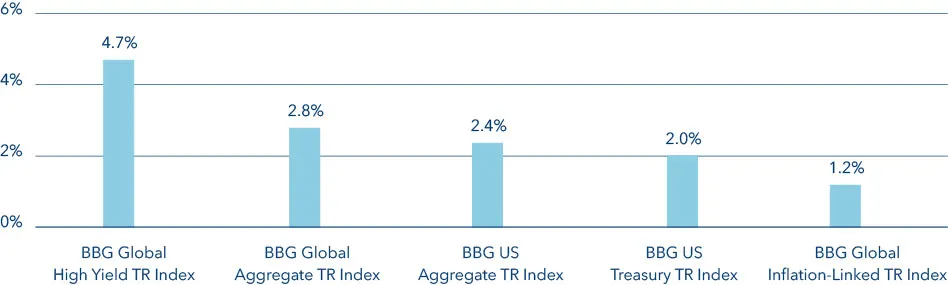

Meanwhile, the performance of bond indices in the first half of the year suggests that the bond market has adapted to the new high-yield environment and could gain traction across the board thanks to attractive yields.

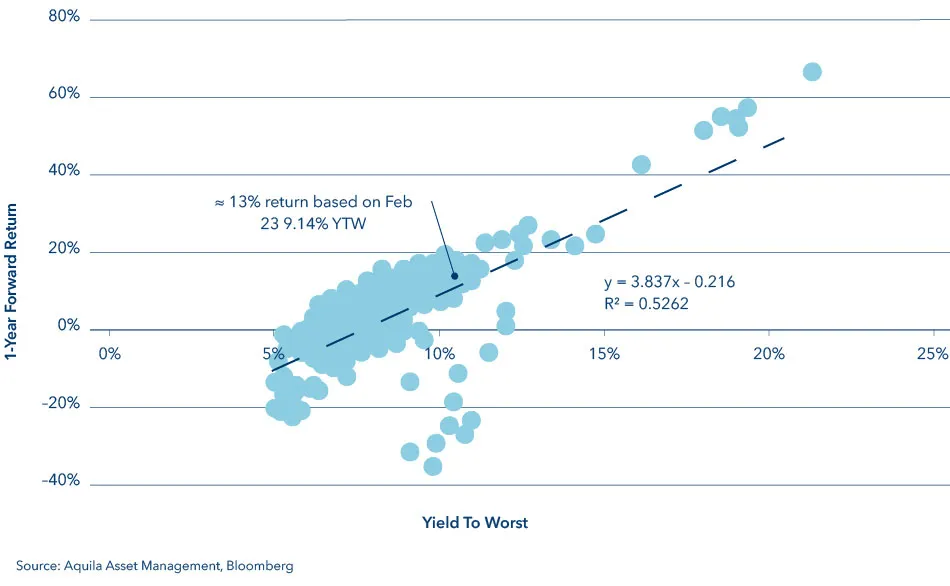

The yield opportunity

Bonds offer an attractive reward for the underlying risk: based on statistical analysis, Global HY names could clinch double-digit returns over the next twelve months.

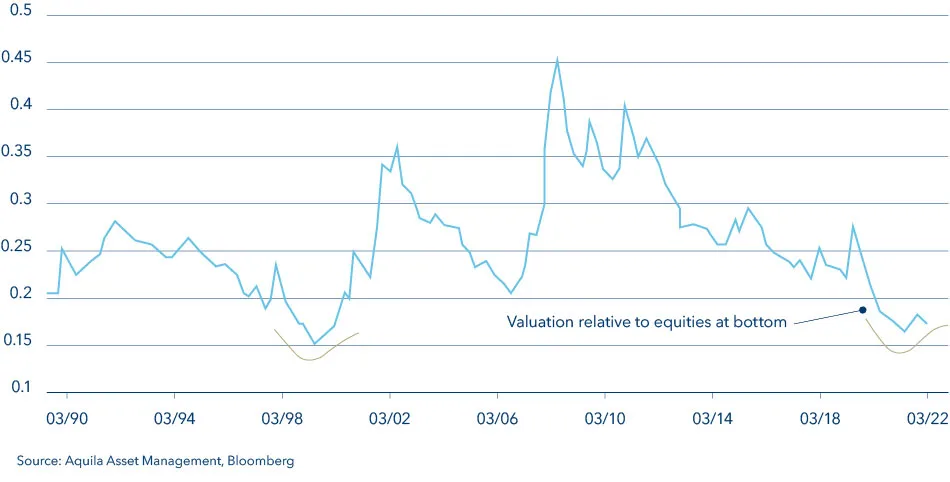

Fixed-Income products can also offer a competitive alternative to equities, with valuations bottoming relative to stocks and better yields for investors.

Lastly, higher-yielding issuers have vigorously deleveraged balance sheets over the last years, entering the current economic phase with a cushion against downturns and higher cost of capital.

Focus on fundamentals, not ratings

Even though ratings provide a service for the stakeholders, they are not the panacea for all woes and may fail to depict the attractiveness of an issuer. First, they are laggard indicators and may fail to anticipate bad outcomes for creditors. Furthermore, issuers may be penalised by country or sector-specific limits that may mislead investors, precluding names because of higher perceived riskiness (due to ratings) than what fundamentals tell.

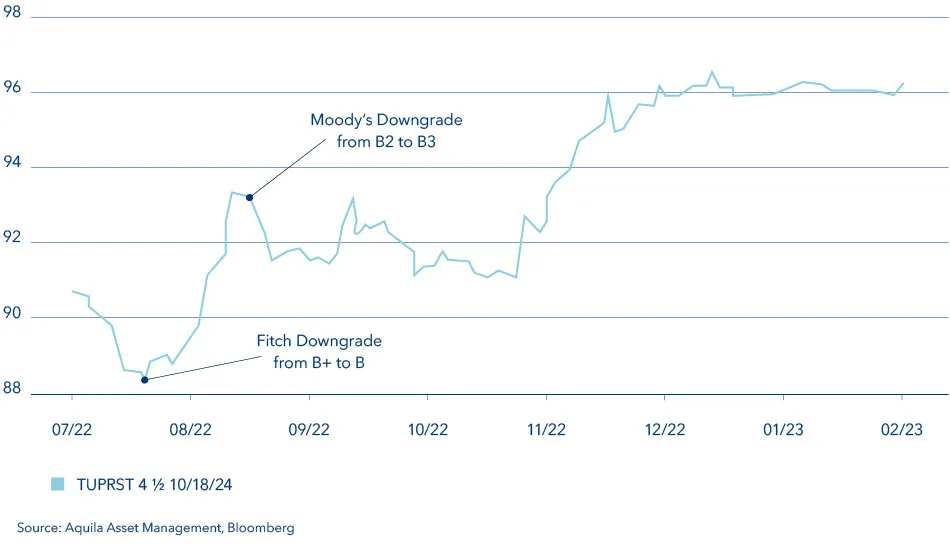

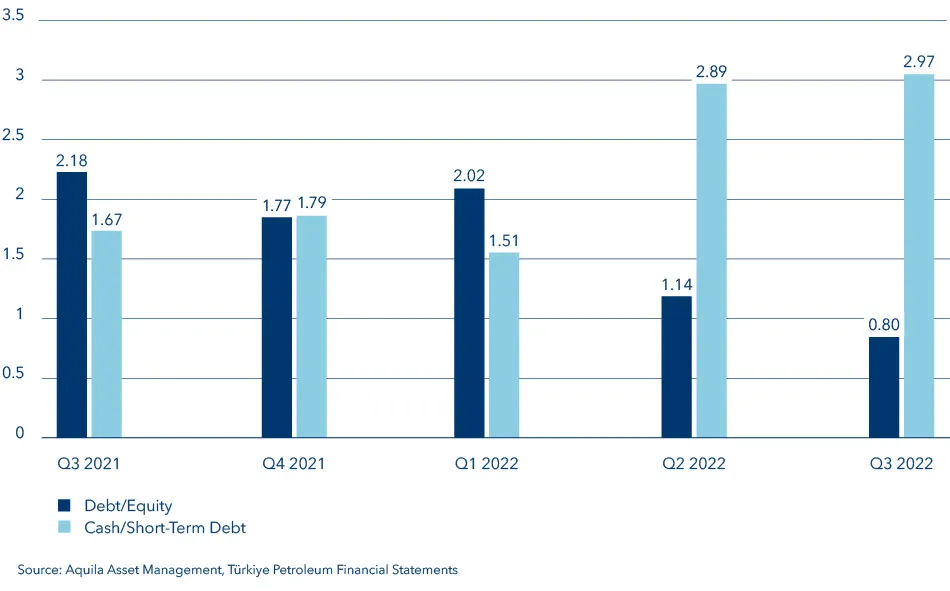

An example may give a better sense of the opportunity cost of basing decisions on ratings: Türkiye Petrol, the largest refinery company in Turkey (7th in Europe), was recently downgraded both by Moody’s and Fitch, the rationale being the lower rating assigned to the government debt, which set the ceiling for the Turkish corporate issuers. Despite that, the company achieved a solid operating performance, improving credit metrics. The positive momentum for the firm was reflected in the bond price (see chart above), which rose despite the actions of the rating agencies.

Because of such dynamics, here at Aquila Asset Management, we focus extensively on fundamentals, ensuring that the issuers we select can survive hard times and thrive in favorable business conditions.

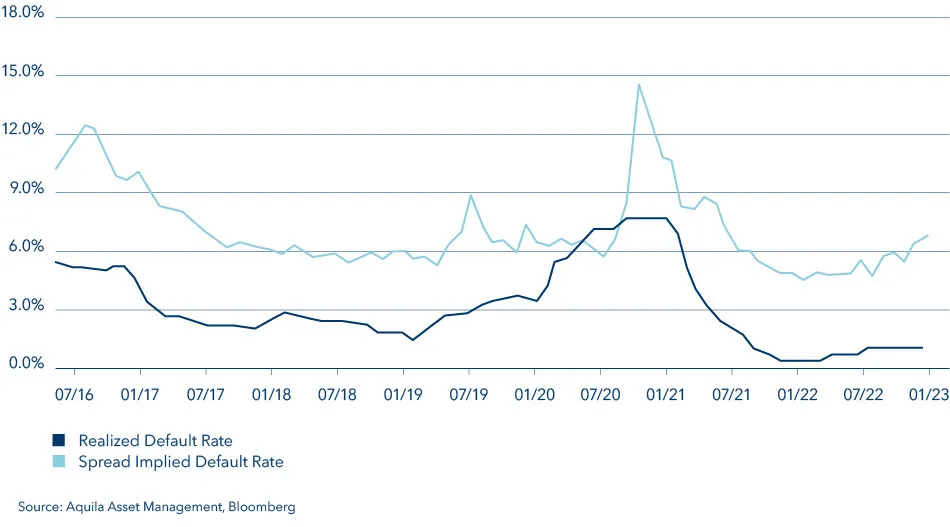

Spread does not mean default

Market participants tendentially overweight the probability of default of an issuer, pushing risk premia higher. Knowing this, disciplined investors can seize attractive returns by fairly assessing the riskiness of the bond.

Based on these premises, we exploit the mispricing and grasp the extra remuneration related to the exaggerated perception of default implied by the credit spreads without compromising the financial soundness of the investment undertaken.

Our pillars for long-term value generation

Aquila Asset Management Ltd. investment approach is based on:

- A global investment universe entailing corporate and sovereign debtors from developed and emerging countries.

- Relative value investing to capture the most profitable opportunities.

- Heavy diversification across multiple layers (country, sector, technical factors, etc.).

- In-depth fundamental analysis.

- Active and opportunistic investment style based on the convictions of team members, a rigorous risk management framework, and clear investment guidelines.

We concentrate our efforts on Hard Currency investments (using the US Dollar as the base currency) and manage duration by positioning the portfolio on the most optimal spots of the various issuers’ yield curves, where we can maximize the benefits of the roll-down effect.

Important legal information

This article is for information purposes only and does not constitute an offer or an invitation to buy or sell financial instruments. The recommendations, assessments and statements it contains herein reflect the personal views of the respective guest author and may differ from those of VP Bank Group. This document is based on information derived from sources that are believed to be reliable. Although the utmost care has been taken in producing this document and the assessments it contains, no warranty or guarantee can be given that its contents are entirely accurate and complete. In particular, the information in this document may not include all relevant information regarding the financial instruments referred to herein or their issuers. Past performance is not indicative of future results.